- Day-ahead prices in gas and electricity rose 58% and 67%, respectively month on month

- Bouts of colder weather in early April and the ongoing situation in Ukraine will likely further spike prices across the energy complex.

Flogas Enterprise (formerly Naturgy Ireland) has today released their monthly report for March 2022, which outlines the latest price fluctuations for natural gas, electricity, oil and carbon along with the reasons behind these fluctuations. The report also forecasts how prices may shift in the coming weeks based on analysis of the global context in which the fuel markets operate.

Lauren Stewart of Flogas Enterprise said of the report “Today, we release the latest of our monthly reports, which offers a valued insight into drivers of the recent fuel price fluctuations. Undoubtedly the past two months have been turbulent, with the invasion of Ukraine impacting prices significantly and many customers feeling the effects of the price changes. The aim of the report is not only to summarise factors influencing prices in recent months, but also giving our customers and other interested parties an opportunity to gain a deeper understanding of the markets.”

The report outlines how fossil fuel prices have been driven by the fact that Russian supply has been called into question. Russia is still honouring their pipeline flow agreements, but security of this supply has created a lot of volatility on the prompt off news that the Kremlin wants gas to be paid in Roubles.

There was limited price bearishness in March given that China (who is the world’s largest oil consumer) went into lockdown across Shanghai to contain the spread of Covid-19. In addition, an Iran nuclear deal could bring much needed supply to the market.

Looking forward, it is expected that bouts of colder weather in early April would increase heating demand. This will likely elevate carbon and natural gas prices further. The carbon market will continue to closely track peace talks between Russia and Ukraine in the coming month.

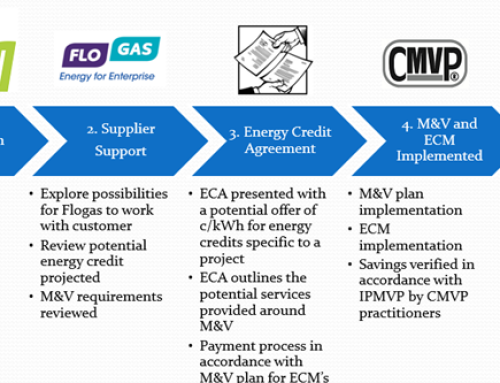

Since December 2021, Naturgy Ireland has been rebranded as Flogas Enterprise after the successful acquisition by Flogas. It has long been a leading supplier of renewable electricity, natural gas and energy services to large energy users across Ireland, Northern Ireland and the UK, with a share of almost 17% of the industrial and commercial natural gas market. Business customers and large energy users can also be provided with renewable gas under the Flogas Enterprise brand.

Flogas Enterprise supplies natural gas, renewable electricity, compressed natural gas and more recently, a range of energy services that include Lighting-as-a-Service, Solar PV and corporate PPAs.

Flogas provides renewable electricity, natural gas and LPG energy solutions to the residential sector and to over 30,000 commercial customers, primarily SMEs, across the island of Ireland and will now be in a position to expand the range of sustainable energy services offered as well as offering larger energy users a broader all-island solution.

For more information on visit www.flogasenterprise.ie

ENDS

Top Line Information from the Report

Natural Gas

Summary:

Day-Ahead prices hit a peak of 515 p/therm early in the month off the back of the Russian invasion of Ukraine. Prices then declined to 218 p/therm towards the end of March upon news that the US would likely provide additional LNG cargoes to Europe. The prompt jumped back up to 270 p/therm upon the Kremlin announcement that gas contracts needed to be paid in Roubles.

Price Drivers:

Prices rose significantly off the back of Russian invasion of Ukraine with many EU energy giants walking away from Russian projects early in the month, most notably Nord Stream 2. Russia is still honouring their pipeline flow agreements, but security of this supply has created a lot of volatility on the prompt off news that the Kremlin wants gas to be paid in Roubles.

Outlook:

10 LNG cargoes are expected to dock at British terminals over the next fortnight, this is 6 more than the same period in 2021. Below seasonal temperatures and low wind generation into early April could bring some additional support to the gas prompt.

Electricity

Summary:

Day-Ahead power prices rose significantly due to a bullish wider energy complex with gas prices rising 58% month on month. Wind generation was low this month averaging at 1,561 MW, this is 44% lower than the previous month averaging at 2,777 MW. The lowest daily average price was 16.34 c/kWh, with wind generation peaking at 3,324 MW on this day.

Price Drivers:

Gas has made up circa 40% of our fuel mix this March. The record highs this commodity has reached is feeding into the electricity price. Wind generation did have a correcting measure on the price in March making up 35% of the monthly fuel mix. Carbon prices began to rise again towards the end of March feeding into the Day-Ahead electricity price.

Outlook:

There is significant offline capacity for April, with reduced capacity at the Moyle interconnector and EWIC entirely offline. Reduced capacity is expected to persist until early May. Wind generation is expected to remain low into the coming month, this could bring sustained bullishness to prices due to increased reliance on the bullish gas commodity.

Oil

Summary:

Brent Crude traded above $100/bbl for the month of March. They dipped below this threshold mid-March due to sings of progress to peace talks between Russia and Ukraine and bearish US inventory data. The EU’s refusal to ban Russian oil imports brought some sentiment of bearishness to the market but prices still maintained well above €100/bbl.

Price Drivers:

Russian oil supply has been called into question given their invasion of Ukraine with Europe making efforts to plug the gap elsewhere. There was also some price bearishness in March given that China, the world’s largest oil consumer, went into lockdown across Shanghai to contain the spread of Covid-19.

Outlook:

An Iran nuclear deal could bring much needed supply to the market. OPEC+ met in early April for the first time since Russia has invaded Ukraine to discuss monthly production quotas for members. They intend to maintain the existing quota of increasing production by 432,000 bbl/day in May.

Carbon

Summary:

The first two weeks of March saw a consecutive decline to prices due to milder weather conditions and financial markets struggling to grasp the impact that the war in Ukraine would mean to prices. à Prices then began to correct upwards due to the impact that the Russian invasion of Ukraine was having on the wider energy complex.

Price Drivers:

Warmer weather in March brought price bearishness due to lower demand for heating. Low wind outturn meant increased demand for alternative power generation resulting in an elevation to the price of carbon. Financial markets were closely tracking any news coming out of Ukraine which was fed into the carbon market causing the price to swing with prices trading €12/tCO2e higher from the start to the end of the month.

Outlook:

Expectations of colder weather into April will increase heating demand and likely elevate carbon prices further. The carbon market will closely track peace talks between Russia and Ukraine in the coming month.